The basic concept of investing can be quite simple at the surface level. Invest X dollars, make a certain rate of return during the year and end up with X dollars plus that return. But what happens next year? Would you earn the same return the following year? The frustrating answer to this question is yes... And no. This is due to the power of “compounding returns”.

Compounding return may sound complicated, but when broken down, the concept becomes much easier to understand.

What is Compounding?

Compounding occurs when an amount is multiplied by a certain percentage, with that result being multiplied by the same percentage, over and over again. This is not to be mistaken with the initial amount being multiplied by that percentage over and over again. This would only bring back a small difference at the start, but after repetitions, the gap between the two becomes larger and larger.

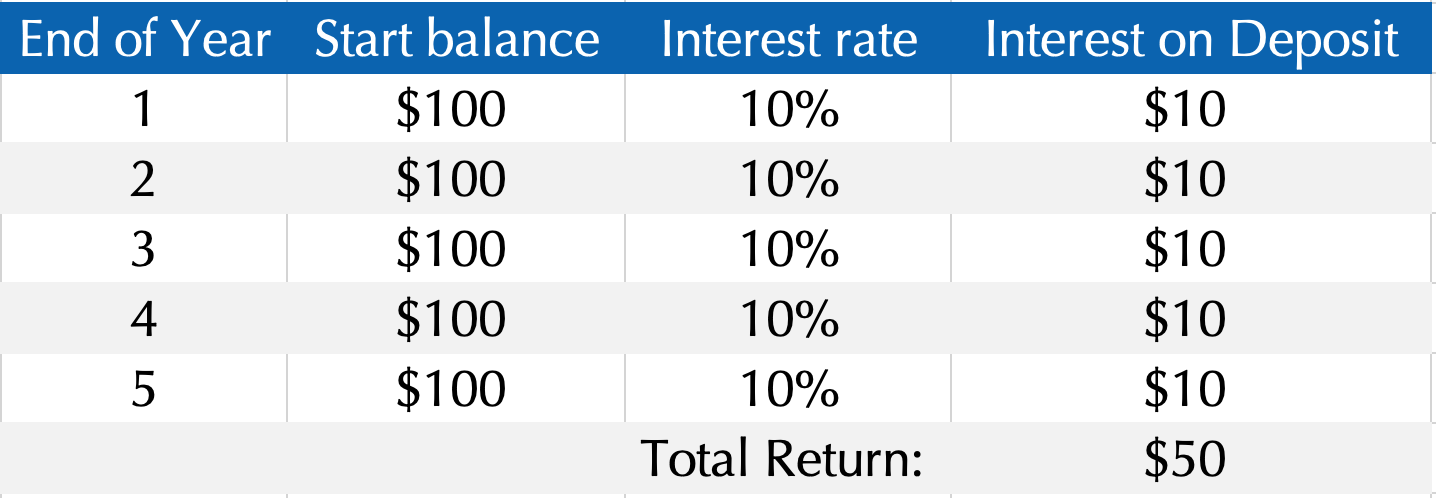

Let’s say you have $100. Upon depositing this money in a bank you are offered 10% interest per year. So logically you would think that after 5 years you would have $50 in interest right?

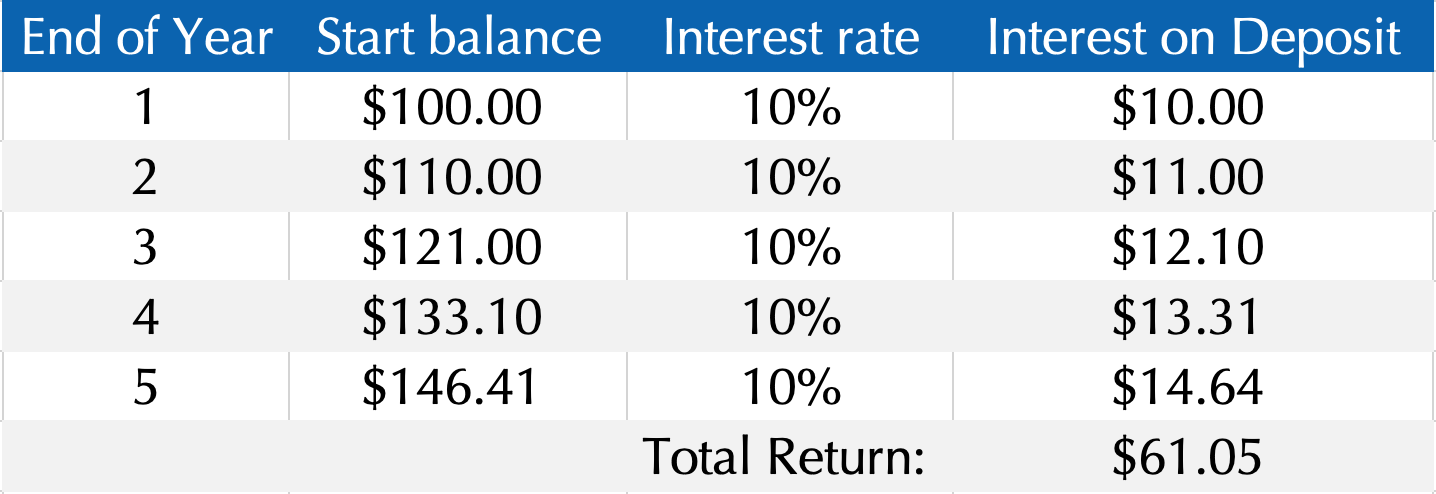

These calculations show the effect of simple interest, where interest is calculated off the initial principal amount of $100. This is helpful when making a rough calculation. However, if the interest is compounding (which it usually is) then this figure is actually wrong. The 10% interest is on top of the amount originally in the account. So after year 1 you will have $110 (your initial amount of $100 + $10 interest). When multiplying this new amount by 10% your interest amount for the following year will actually be 11$ instead of $10. More simply depicted below.

At a first glance, the $11.05 difference between the two does not look like much. But over a longer time period, the gap becomes larger and larger due to the power of compounding interest. In terms of a bank deposit, compound interest sounds terrific. But the same thing also applies to Debt. If you have a credit card that charges a rate of 12% per year, then the following year you will be charged 12% on top of the interest already owed making compound interest a double-edged sword to watch out for.

This is all well and good but how does compounding interest increase your KiwiSaver balance when your account doesn’t earn any interest?

Compound Interest Vs Compound Return

Because your KiwiSaver fund is an investment rather than a deposit at a bank, you do not actually earn interest on your sum of money. What you do gain (hopefully) is the return on your investment. When swapping out the term “compound interest” with “compound return” you can see how this concept is relevant to your returns. Though the return on investment lacks the definite gain or constant nature of interest, historical data can indicate an expected rate of return which can be used to calculate compounding returns on your KiwiSaver.

Say the expected rate of return on your KiwiSaver type each year is 10% and your balance is at $1000. The green line represents the returns each year calculated on your principal amount, whereas the white line represents returns calculated on the combination of your principal amount + all returns gained previously (assuming you leave all returns invested). The green line shows your KiwiSaver account value to increase by the same amount ($100) per year, while the white line shows it to increase more and more as the years go by.

After 30 years, compounding returns will have helped your KiwiSaver account reach a balance more than $13,000 higher than that of the value it would be if it was just returning 10% of the initial amount each year. These calculations exclude all contributions from yourself and your employer for the sake of a simplified explanation.

Does My KiwiSaver Account do This?

Short answer - Yes. Your account manager automatically reinvests your returns to help compound further returns. Terms and conditions state that you are not able to withdraw your investment unless it’s for the designated purpose such as retirement or a first home deposit. This means that you are actually unable to withdraw any returns on your principal amount, unlike other investment options. This means that all returns made on your investment go straight back to work on compounding larger returns as your balance grows over time. This differs from many other investments as it is usually very easy to withdraw returns and use them elsewhere if so desired.

Having compounding returns on your KiwiSaver account makes it all the more important that your money is invested in the right fund for you. Let’s take a couple of funds from the same provider for example.

Say we have both the ANZ balanced fund and the ANZ growth fund for a comparison.

Their past 5 year average returns were 6.32% and 8.32% respectively. At surface level, it looks like there is only a 2% difference in returns. On an initial $1000 investment this is a mere $22 difference after year 1. But 20 years down the line, after the compounding rate of return has had a chance to make a bit of an impact, that $22 gap is now $1539. That means if you were placed in the balanced fund by your provider then you’re now $1517 down (and that’s assuming you only had $1000 in your account and made no contributions).

This is an unfortunate reality for so many KiwiSaver scheme participants who are simply not in the right fund to suit their specific needs. The crazy thing is, it doesn’t have to be like that.

National Capital specializes in connecting kiwis with the fund that is going to be the best for them and their goals. So if you’re interested in putting compound returns to work in the most optimal way possible then give our HealthCheck a whirl to work out which fund will serve you the best.