Kiwis from all walks of life have been able to save for retirement and buy their first home thanks to the introduction of KiwiSaver in 2007. Since then, it has been deeply ingrained in the culture of the New Zealand financial system.

However, there is a significant portion of people who still do not have a clear idea of how it operates. In many instances, this is a result of erroneous information or modifications that have been made to KiwiSaver since its introduction.

There are still some misconceptions about what KiwiSaver is and how it works. That is despite the fact that millions of New Zealanders are participants in the program. In this article, we will discuss some prevalent misconceptions & falsehoods around KiwiSaver, and then we will dispel them.

5 common misconceptions about KiwiSaver are:

- It’s just for older people.

- If you die, the government will get your savings.

- It’s only for people over the age of 40 and a specific income.

- You can only withdraw after retirement.

- You must be an employee.

1. KiwiSaver is just for older people

Everyone can participate in KiwiSaver (well, nearly everyone). Regardless of age, you are eligible to join as long as you are a New Zealand citizen or permanent resident. If you are under 18, you will have to join through your KiwiSaver scheme rather than an employer. Those with a temporary, visitor, work, or student visa cannot join.

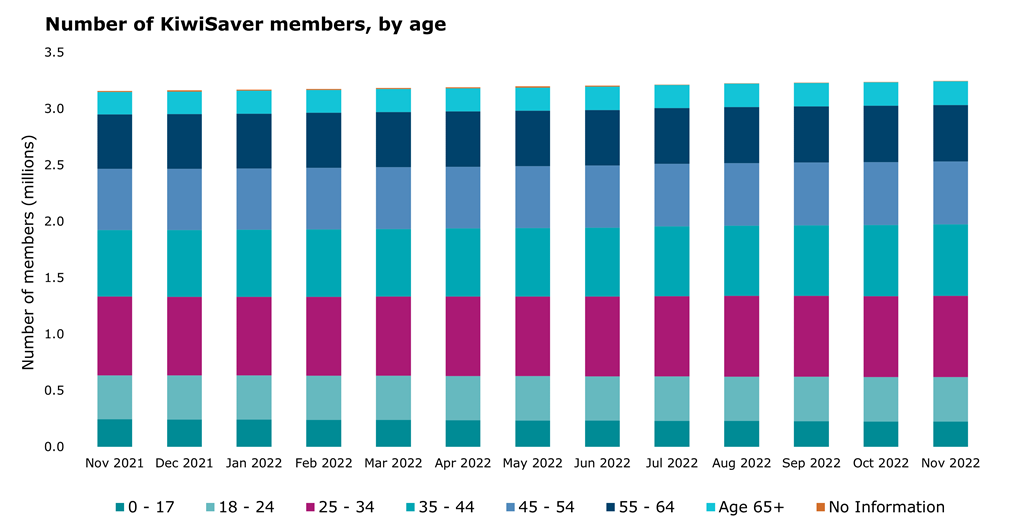

Graph Source: (IRD)

As of November 2022, there are:

- 223,476 members aged between 0-17

- 393,984 members aged between 18-24

- 721,547 members aged between 25-34

- 634,514 members aged between 35-44

- 559,378 members aged between 45-54

- 500,641 members aged between 55-64

- 208,664 members aged 65+

Starting your contributions at an early age can make a significant difference in the long run. Even if you are years away from reaching retirement age. You also have the option of withdrawing the money from your KiwiSaver account to assist with purchasing your first house.

The best time to join was yesterday and the second best time is today. Saving and investing today will make a significant contribution to your retirement plan and finances later down the line. In fact, the earlier you start, the more chances you have to accumulate additional wealth and returns on your investment.

2. If you die, the government will get it all

Wrong! There is a misconception that your money goes to the government or possibly even your employer when you pass away. It is not the case at all. When you pass away, the funds in your KiwiSaver account are added to the rest of your estate. Along with any other assets you might have, it will go to your next of kin or whoever you’ve chosen.

Including your KiwiSaver investment in your will is the most reliable way to guarantee that your funds will be distributed in accordance with your wishes when you pass away. Without a will, the process can get complicated, expensive and long (between 6 to 24 months). We break down the scenarios that can happen to your account if you pass away in this article.

The government actually contributes up to $521.43 each year you’ve contributed a minimum of $1042.86.

3. KiwiSaver is only for people over the age of 40 and a specific income

As briefly touched on, this is also false. Anyone can join KiwiSaver, up until the age of retirement (currently 65). As long as you are a New Zealand citizen or have a permanent residency here. Even if you leave the country, your KiwiSaver investment is expected to provide returns in the long term.

There’s also rumours that KiwiSaver is only for people with an income above $60,000 per year. False again! In fact, KiwiSaver has contribution options that are perfect for everyone – from full-time workers to retirees on a modest income. Plus, KiwiSaver doesn’t restrict your ability to earn extra money in other ways (like self-employment or freelance work). So whether you make $20,000 or $200,000 annually, joining KiwiSaver is all the same.

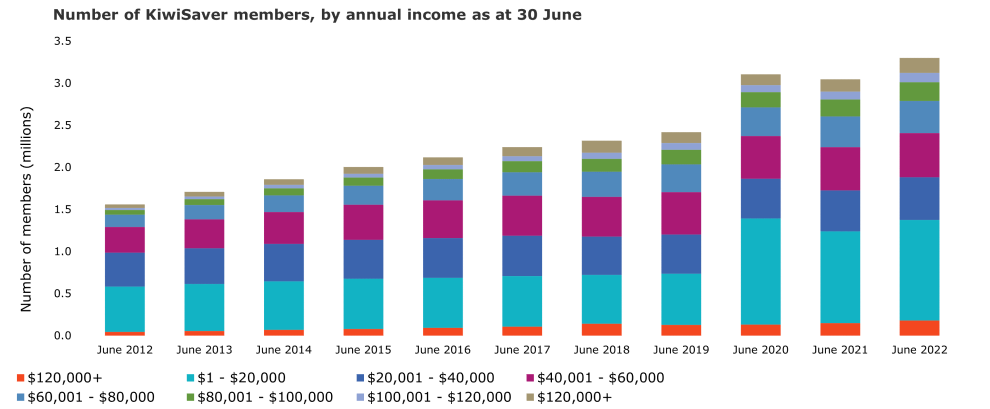

Graph Source: (IRD)

As of June 2022, there are:

- 1.2 million members earning between $1 to $20,000 annually.

- 523,507 members earning between $40,001 to $60,000 annually.

- 384,503 members earning between $60,001 to $80,000 annually.

- 220,221 members earning between $80,001 to $100,000 annually.

- 111,040 members earning between 100,001 to 120,000 annually.

- 178,735 members earning more than $120,000 annually.

If you are self-employed, a stay-at-home parent, or even if you have retired early, putting as little as $20 per week into a KiwiSaver account will get you $521.43 of government contributions annually – with only $1042.86 of your own savings a year.

Surprisingly just 59% of us contribute to KiwiSaver. The remaining 41% are presumably passing up opportunities to receive free money.

4. I can't touch the money until retirement

The point of the scheme is in fact to support the individual once they reach retirement age. although, there are a few circumstances where you can withdraw your savings before retirement. Note that certain criteria must be met and followed by supporting documentation in order to be eligible for a withdrawal.

It is possible to take out money from your KiwiSaver account to help you purchase your first home. In today’s market, most first-home owners take full advantage of this possibility.

If you’re having trouble paying your bills, you may also be able to take money out due to financial hardship.

You can also withdraw your savings or transfer them when emigrating permanently out of New Zealand.

5. KiwiSaver is only for employees

No, it is not reserved solely for employees. Joining KiwiSaver does not mean you have a job to be eligible. As a parent, you can enrol your chile into KiwiSaver as early as you want.

You can also join KiwiSaver self employed.

Non-employees will not be eligible for the (minimum 3% of salary) contribution made by employers. However, they will be eligible for the yearly contribution made by the government, which is practically free money.

Conclusion

The KiwiSaver scheme is by far the most widespread investing option available in New Zealand, with over 3 million participants. It is inevitable that it will garner a plethora of misunderstandings, in addition to a diverse array of perspectives.

Knowledge is power when it comes to investing, and National Capital is here to help assess your Kiwi Saver options. We’re qualified to give advice on the best KiwiSaver funds available and bust any myths and misconceptions.