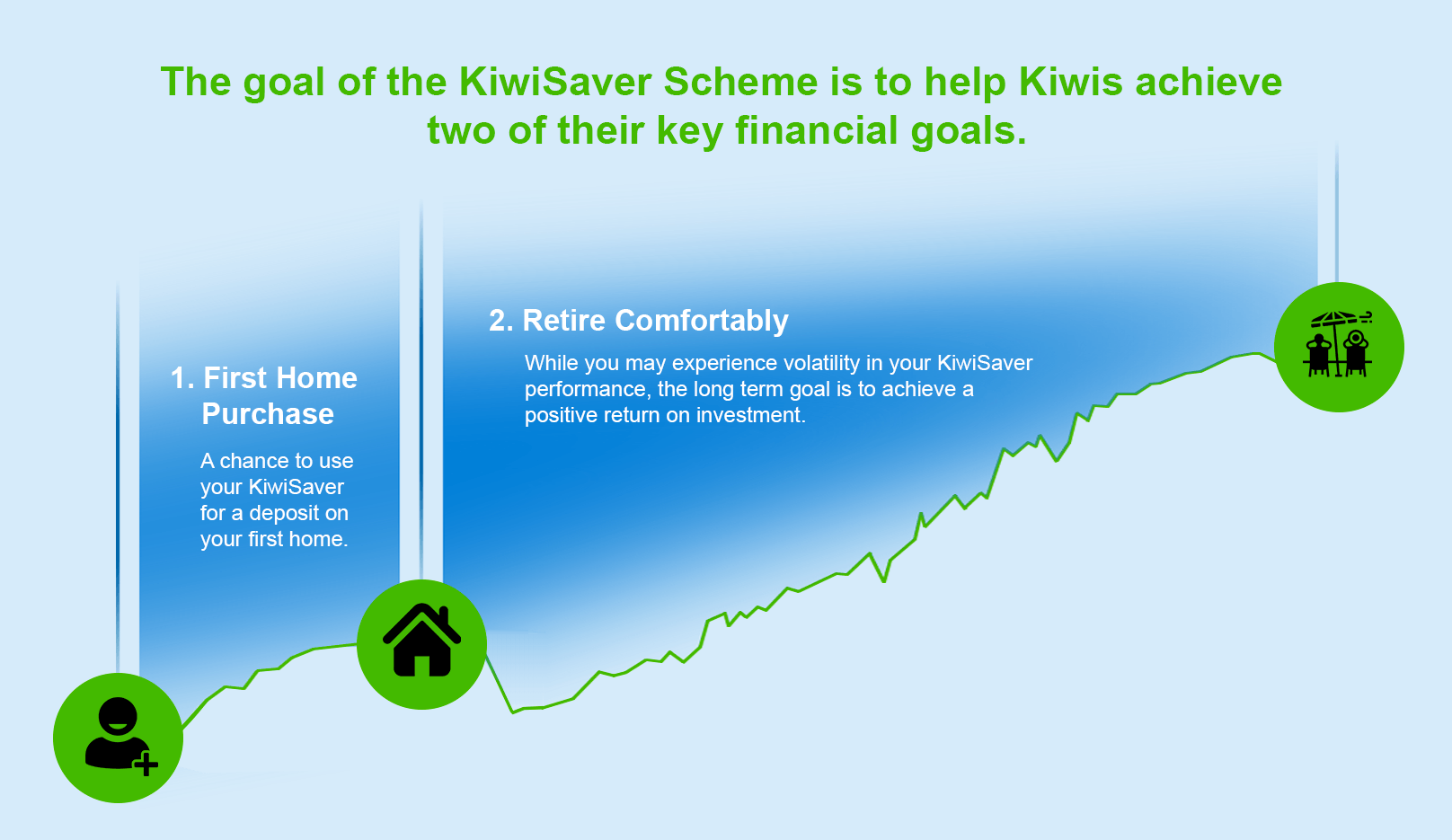

| Objective: | KiwiSaver is a savings and investment initiative designed to help create a sustainable retirement plan. |

| For Who: | All New Zealand residents of any age are eligible for KiwiSaver sign up, regardless if they work or not. |

| Contributions: | Employee: 3%, 4%, 6%, 8%, or 10% of salary. Employer: Minimum 3% of salary. Government: 50 cents on every dollar up to $521.43/yearly. |

KiwiSaver sign up may feel a bit confusing, and you may not know what questions to ask. But here at National Capital we believe in giving more power to the client. We will go over the most important information you need to know as someone joining KiwiSaver or an existing investor that wants to know more. Every one from KiwiSaver self employed to someone nearing retirement can benefit.

National Capital is specialised in investment research. We have a list of all the KiwiSaver companies on this page. There are different considerations when choosing KiwiSaver for someone planning to use their savings for retirement as compared to someone who is looking to use them for a First Home purchase. If you are planning to use them for retirement, you need to take into consideration your retirement income goals, the lump sum you need at retirement, and your current balance and rate of savings. You will also need to take into consideration your capacity and tolerance for volatility.

We have tried to answer the question of “How does this KiwiSaver choice compare to others?”. Click on the name of your current KiwiSaver company at the bottom of this page to see how it compares against others in the market and get an indication if it is the appropriate one for you.

However, please note that the information on the pages linked from here is not personalised financial advice for KiwiSaver sign up. If you want advice based on your own circumstances and goals, follow the HealthCheck application on our website. National Capital was founded in 2018 and now advises Kiwis on over $70 million of their KiwiSaver savings. We are based in Auckland, but serve clients all over New Zealand. We provide free advice, with the goal of empowering one million kiwis to become financially secure.

Whether you're thinking of joining KiwiSaver for the first time, in KiwiSaver self employed, or already in a company recommended, here are some quick links to the most common queries:

Our core function is research and advice. Therefore, whether you're a long-time investor or just thinking of joining KiwiSaver, you can benefit from our specialised insight. It only takes a few minutes to enter your detail and get your KiwiSaver recommendations. We've helped Kiwis from all walks of life make decisions tailored to their goals and circumstances. From self-employed to people looking to switch from their default KiwiSaver.

We are a financial advice company specialised in KiwiSaver research. And guess what? We provide FREE advice with the goal of empowering Kiwis to take ownership of their financial security and freedom. We currently have a KiwiSaver list of 14 providers which we work with and recommend based on your circumstances.

Are you ready for National Capital to check the health of your KiwiSaver?

1. HealthCheck / 2. Personalised Recommendations / 3. Decision

A combination of professional financial advisers and the latest technology deliver tailored recommendations, at no cost to you! Follow our 3 simple steps.

It should take you only 10 to 15 minutes to complete the Healthcheck. This gives us what we need to compare your current situation with opportunities to maximise your investment.

Our thorough analysis delivers tailored recommendations suited for you. Based on your goals, you will get recommendations on the most appropriate fund and overall KiwiSaver option.

Our services allow you to make an informed decision amongst all the KiwiSaver options available. You can ask questions, decide to proceed with our recommendations, or stick to your current situation.

Should you wish to apply our recommendations, National Capital makes the switch a completely hassle-free experience.

Before or after joining Kiwisaver, there are multiple ways to see which KiwiSaver option is best for you. Here at National Capital, we provide a HealthCheck to determine how financially tolerant you are and your capacity to save. National Capital’s HealthCheck takes into consideration your goals and how you react to changes within the market. Depending on whether you are buying your first home or retirement, talking with a financial advisor will allow you to make the best decision.

In truth, all KiwiSaver firms are held to a high standard by financial regulators. For many Kiwis when joining KiwiSaver or a few years in, there is very little difference in results. The same goes for joining KiwiSaver self employed or with a company, they all accommodate new customers similarly. Of course, we can recommend the best option for you from KiwiSaver sign up at a young age. However, you will start seeing a significant difference in results when your balance is relatively high.

For example, when your total savings balance is $10,000, an additional 1% in yearly returns equals $100. This is a figure you’d expect in the early years after KiwiSaver sign up. Everyone would take an extra $100 every year if offered, of course. However, it is not significant enough to worry too much about.

Now, let’s assume you’re in your 50’s and have accrued a balance of $500,000 in your KiwiSaver. That additional 1% in yearly returns equals $5000 of potential returns. In this case, KiwiSaver sign up with the best scheme can end up generating a significant amount of additional returns.

Before KiwiSaver sign up, this is a valid question to ask. The only money which is taxed is the earnings gained from your KiwiSaver returns each year. This means that you aren’t paying out of pocket for the returns, and is taken off the amount made within the year from the account. Any money that is withdrawn from your account is tax-free.

KiwiSaver is taxed like any other investment fund type here in NZ. When joining KiwiSaver you will determine your Prescribed Investor Rate (PIR) to determine your tax rate. As a New Zealand resident, you will typically fall into one of the following:

The good thing is that once you set your PIR, whether you joined KiwiSaver self employed or through a company, you don’t need to manually do your taxes on it. Any payable tax is automatically taken from your KiwiSaver balance depending on your investment returns.

Depending on your provider, your KiwiSaver fees may vary. This includes annual management fees and fixed quarterly payments. Fees are based on your savings amount, and the services your fund provides. It is in your best interest to compare the fees with the returns when comparing funds. Although you may receive higher returns, they may be outweighed by the fees charged. Check with your provider to see what you're paying if you aren’t sure. You can also contact National Capital to help track down these figures for you.

Over the past few years, fees have decreased with a push from various government actions. However, it is understandable for a KiwiSaver firm to charge a management fee in order to provide the service. After all, it is a business with expenses and profit expectations. In order to hire the best financial analysts and investors to manage our funds, they need to pay good salaries.

Importantly, during KiwiSaver sign up, you should not mistake higher fees for better performance and vice versa. There isn’t a clear correlation between KiwiSaver fees and performance, thus you need to look at other factors when selecting. Lastly, there is no difference in fees whether you are joining KiwiSaver self employed or through an employer.

No, KiwiSaver, much like other investments is not guaranteed to give specific returns. However, we can look at long-term averages to get an indication of the range of expected returns from different types of funds. Of course, KiwiSaver performance data will fluctuate over time.

These are the average KiwiSaver returns per annum for the last decade for the major funds:

Whether joining KiwiSaver self employed or in a company, you shouldn’t neglect the fact that investments can go negative. However, history will tell us that long-term investment has an upward trend.

You may ask if that’s the case then when should I worry? You can start taking action if you see your KiwiSaver underperforming competitors on a consistent basis. That may be confusing to keep track of and that’s where National Capital comes in. Whether you’re in KiwiSaver self employed or have been put into a company default provider, we can help.

KiwiSaver sign up, like any other investment, is not insulated from market volatility. This means that your money can go up or down in value. Therefore, the short answer is yes. You can lose money on KiwiSaver. When joining KiwiSaver, this is important to know so that you can make the right decisions when your balance is in the red.

However, it is not as doom and gloom as it sounds. Companies in the main global markets, in general, go up and down in value all the time. Reasons can vary from news articles to bad ad campaigns, and global pandemics like Covid-19. No matter how tech-savvy the financial industry gets, it is impossible to predict and guarantee investments as totally risk-free. KiwiSaver firms work full time in researching market trends and analyse companies to ensure they have a sustainable business model.

Additionally, professionals working in a KiwiSaver company invest your money in a way designed to spread the risk. Whether this is across different companies, industries, or markets. For example, looking closely at the breakdown of your fund, you will see many companies across multiple industries. KiwiSaver firms structure your investment this way particularly to spread risk and minimise the impact of unforeseen downwards trends.

Source: Google Finance

In conclusion, as company valuations are susceptible to downgrades, you can lose money on the scheme. However, history tells us that investing in stable markets, KiwiSaver has grown in value in the long term. Let’s take a look at the NZX50 Market Index from inception in 2003 to the end of 2021. We can see dips and drastic loses along the way but the value over those 18 years has increased 585%. This leads us to the ultimate point in this topic. Timing is everything.

Make a Video appointment with one of our Financial Advisers.

We've helped hundreds of Kiwis sort out their retirement plan. Click the button below to set a 30-minute video call appointment.