The safest place to invest your savings is somewhere you feel most comfortable and that helps you achieve your financial goals. No matter where you invest, you will always be facing risks. However, there are ways you can reduce these risks.

The FMA and Colmar Brunton, who surveyed 1,000 New Zealanders on their investments, found that the five most popular investments are:

- KiwiSaver 67%

- Life Insurance 37%

- Alternative superannuation 14%

- Managed funds or unit trusts 7%

- Portfolio managed by a professional investment advisor 5%

As we can see, only a small amount of people didn’t invest their money into KiwiSaver.

This is because it is a great way to invest and grow your money with less risk.

Don’t delay, set up a financial plan, and start optimising your investments now!

So is KiwiSaver for you?

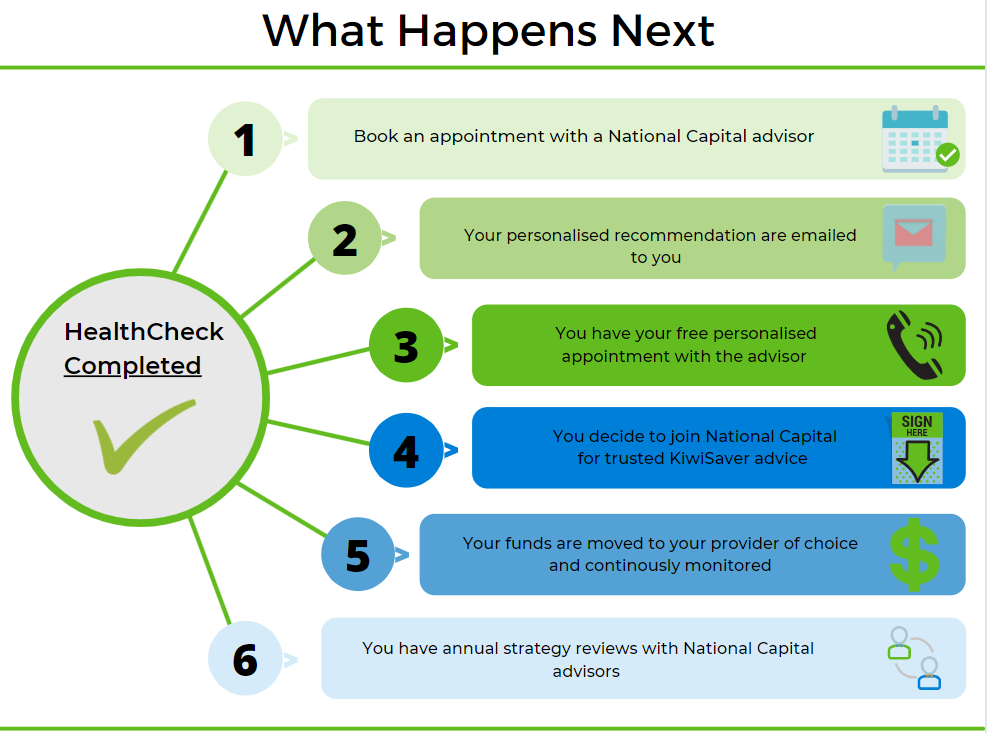

Whether or not it is the right place for you to invest depends on your personal circumstances and goals. For most Kiwis, a KiwiSaver account is a great investment strategy, but as each person’s financial situation will be different it is not possible to give one clear answer. To help you analyse your situation you can use National Capital’s no-cost KiwiSaver HealthCheck which gives you a detailed breakdown of your current financial situation and helps you develop a plan to achieve your goals. This can also help you figure out how much money you want to invest and how much you want it to eventuate into.

What does KiwiSaver offer you?

It offers you not only free government contributions and employer contributions but the benefit of compounding interest as well. Compound interest is when the returns from your investment are reinvested and you then make returns on your returns. The government invests $0.50 for every $1 you invest into your KiwiSaver account up to a maximum of $521.43 per year. That’s a bonus of $500 every year just for investing your money! Employers also contribute up to 3% if you contribute 3% of your salary. This means that because of compounding interest you make money not only on your own investments but also on the government and employer contributions to your KiwiSaver fund. Also, even if you are self-employed, you can still sign up and receive the government contribution if you invest in it yourself.

Investing small sums regularly into your fund will make a significant difference to the future of your investment’s growth.

Risks you Face When Investing and How to Reduce Them

Like any investment KiwiSaver also has risks, but there are strategies you can use to reduce them. Depending on what type of fund you invest in there are different risks you may face. To help you work out which fund is best for you use National Capital’s Free HealthCheck. The risks that investors may face are:

- Equity Risk

- Interest Rate Risk

- Currency Risk

- Diversifiable Risk

- Business Risk

- Financial Risk

- Investment Manager Risk

- Volatility Risk

Now if this seems overwhelming, don’t freak out. There are many strategies available to deal with these risks. And remember as they say, “no risk, no reward”.

Before you invest in anything, it is important to do your research, know the risks you face, and how to deal with them. Getting sound financial advice before making any decisions is also advised. “Investing doesn’t really have a one-size-fits-all approach, even if people have similar goals, they’ll likely need to take different actions to achieve it. That’s why we recommend getting personalised advice and recommendations,” says Clive, Director of National Capital, a trusted financial advisor.

- Market Risk – Investment market risk is how markets perform. This is dependent on the overall economic conditions of a country and for international markets, the world.

- Equity Risk – The risk that share prices will go up and down, causing losses or profits.

- Interest Rate Risk – The risk that an increase or decrease in interest rates will affect stock prices.

- Currency Risk – Exchange rates going up or down affecting investments in foreign companies, or companies that have suppliers or customers in foreign countries.

- Business Risk – The risk of investing in businesses, they could fold or run at a loss.

- Financial Risk – The risk that a company’s financial structure could negatively affect its investment value. For example, it could operate in a way that if anything happens its cash flow cannot cover its debts.

- Political Risk – That changes in policies or economy can affect investments. For instance changes in trade barriers, legislation or taxes.

- Volatility Risk – This is the fluctuation of markets, stocks, or investments, prices can go up and down due to various factors. An example of a market event that could cause prices to change would be the recent Covid-19 outbreak and corresponding lockdowns causing stock prices to plummet.

- Specific Risk – This is a risk unique to businesses, individual stocks, and industries. It is the risk of losing money due to a company or industry-specific hazard.

- Investment Manager Risk – The risk that your investment manager can make mistakes, be negligent or incompetent, and cause losses. Or the risk of management changes and investment style changes affecting your investments.

With so many risks, how can you minimise your investment risk exposure? This is where risk reduction strategies and diversification come into play. Before you decide on your investment and risk management strategy, however, it is key to understand how emotions can affect your investing. Watch this video from Edward Jones to better understand how emotions affect investment decisions and risk levels.

Knowing and understanding your emotional capacity as an investor and your personal investment strategy is key to making safe investment decisions.

Risk Reduction Strategies

Diversification is a strategy to reduce investment risks. It does this by investing your money into multiple industries, shares, and markets. This allows you to “not put all your eggs in one basket”, meaning that if a certain stock or industry crashes you have not invested everything into it and can still rely on your other investments to safely carry you to your financial goals. Strategies on how to reduce risks:

Market Risk – this can be reduced by diversifying your investments into multiple markets and countries.

Equity Risk – this can be reduced by doing proper research, diversifying your portfolio, and having a long-term investment plan in place.

Interest Rate Risk – this can be reduced by diversifying your portfolio investments and investing overseas.

Currency Risk – can be reduced by diversifying investments, investing in multiple currencies, companies, and countries.

Political Risk – this can be reduced by diversifying your portfolio and investing in multiple countries.

Business Risk – can be reduced by diversifying your investments and investing in multiple companies.

Financial Risk – can be reduced by researching companies first and investing in multiple businesses and diversification.

Volatility risk – can be reduced by investing in investments that align with your income, financial plan, timeline, and volatility tolerance. To figure out your volatility tolerance and what type of investor you are you can take National Capital’s Free HealthCheck.

Specific risk – can be reduced by diversifying and monitoring your investments, or investing in low-risk investments like fixed interest securities.

Market, Equity, Interest Rate, Currency, Political, Business, Financial, Volatility, and Specific risks can all be reduced by basing investment decisions on proper research, diversification, and having a financial plan to deal with them in place.

Investment Manager Risk – This can be reduced by making sure that you research and trust the manager/company you choose to use to invest your money with and create your financial plan/portfolio.

It is very important to find a competent investment manager and advisor that has the same principles you do. You should research and find out exactly who is going to be managing your money and how. However, in order to do this, you may need to spend hours online searching for the specific information you need to make this decision. Also, while many investment managers and companies might appear the same, if you look at the finer details, they can actually be quite different. There are different investment philosophies managers can follow such as active, passive, ethical, or more. They may be a local or international investment services provider. As providers have many differences, picking the ‘best’ one is not as simple as just looking at their fees and picking one with the lowest fees. It takes a significant amount of time and research. Fear not however as the National Capital team is here to help.

National Capital is the top company in New Zealand when it comes to the number of KiwiSaver providers they work with and the number of funds researched. They currently work with 14 different providers who have over 200 funds among them. That covers close to 60% of the KiwiSaver funds out there. National Capital offers a no-cost advisory service to help you find out which provider and fund is best for your needs. Their team of trusted experts does all the background research for you and takes into account your personal circumstances when offering advice.

So, although you can do all the research yourself, why not use National Capital’s complimentary service, as they are paid by KiwiSaver providers you get all the benefits of their HealthCheck free of charge. You can take this at your convenience and get the assistance of and advantages of talking to a real advisor about your specific needs.

{{cta(‘a8bff18e-b460-432a-90ca-90175772e648′,’justifycenter’)}}

So, why should you trust National Capital KiwiSaver Advisors?

National Capital has helped Kiwis optimise over $70 million of their KiwiSaver retirement savings and over 1000 Kiwis now have peace of mind about their savings after using National Capital’s Free HealthCheck process.

How much risk should you take?

This question has no ‘one fits all answer’, it depends on your specific situation.

Once you know what type of investor you are you can invest in the correct investment types for your circumstances and market risk should not affect your long-term investment plan and goals. Market dips are usually short-term and so long-term investments are generally unaffected.

Before you decide on the risk amount that you can withstand, you need to understand capital loss risk and market volatility. Capital loss risk is often confused as being the same as market volatility, however, they are completely different things.

Capital Loss Risk – The risk of losing the initial money you invested and not being able to recover it.

Market Volatility – the short-term up and down changes of investments, stocks, and markets.

The number one rule of investing is to never lose money. But how do you do this? Through diversification, research, a financial plan, and trusted financial advice. By having a financial plan in place and sticking to it, you can avoid the potential effects of market volatility and the risk of capital loss.

To decide how much volatility and risk you can tolerate you need to look at what type of investor you are. If you are a conservative type investor you will want lower-risk investments, if you are an aggressive investor then you will want a higher risk higher reward type of investment. By finding the right balance between risk and returns you can maximise your investment returns to achieve your financial goals.

Need Help?

Financial advisors National Capital can help you pick the right strategy that minimises your risks and helps you find the safest place to invest your savings. By analysing your personal situation National Capital can help you build a plan to achieve your financial goals and recommend a fund best suited to your needs. As part of National Capitals recommendations for you they offer:

- In-depth Research – Their team researches 100+ different KiwiSaver funds, from asset allocation to investing approaches.

- Answers – Any questions you may have about investing in KiwiSaver can be answered by their trusted advisors.

- Monitor your Investment – They constantly monitor your provider and investment as well as the market environment.

- Their Expertise – their team specialise in Investment and research.

- Free Service to you – They offer you their independent advice and services free of charge as they are paid by the KiwiSaver providers.

- Save you Time – They do all the research and hard work for you so you can focus on other priorities in your life.

National Capital can help you find the safest place to invest your savings today, and plan for the future ahead. They can help you take control of your money and leave your money worries behind. #onelessmoneyworry!

National Capital operates online and gives you free recommendations with the goal of helping 1 million Kiwis become financially secure.

{{cta(‘a8c2d0a9-7f60-4a93-8ba4-7e948ac64124′,’justifycenter’)}}

National Capital is a financial advisory firm based in Auckland, New Zealand that provides personalised investment advice to its clients. Its mission is to help one million Kiwis become financially secure using technology and the principles of pūataata (transparency), tikanga (ethics) and taurikura (prosperity).