We’re here to help find the best KiwiSaver fund for you. Let’s start by providing you with a comparison report of your existing fund.

It's important to check the health of your KiwiSaver fund and understand its position within the market. Submit the form below to view a simple graphic report of your fund.

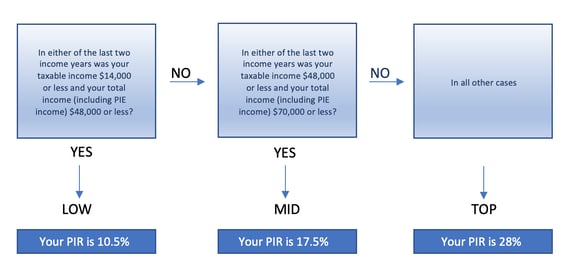

As mentioned above, the amount of KiwiSaver tax you pay is based on your Prescribed Investor Rate (PIR) with an upper ceiling of 28%.

Your PIR for the current tax year depends on how much you earned in the previous two tax years. Upon joining KiwiSaver, it’s your responsibility to tell your provider the correct rate, so if you are still unsure, here is a simple tool to help you calculate your PIR.

The Scheme provider pays the tax on your behalf. To do so, they cancel a number of units you have invested, in order to fund the amount payable to the IRD during the quarter that the tax payable falls on.

Income Tax Rate vs PIR

It is important to understand that your PIR may be a different rate from your income tax rate.

You pay income tax to IRD based on your yearly income for the year. The PIR on the other hand takes into consideration your lowest income in the last two income years. Additionally, the bands & minimum and maximum rates for your Income Tax and PIR are different.

Wrong or missing PIR

Upon setting up KiwiSaver, if you do not provide your provider with a PIR, you will be charged tax at a default rate of 28%. This part of the law has not changed.

However, the IRD has now put systems in place where they will calculate your PIR themselves and ask you (via your provider) to correct your tax rate if you have registered with an incorrect rate. Should you be due a refund, you will now get paid that money back.

The refund will be paid directly to your KiwiSaver provider and used by them to buy more units on your behalf in your chosen fund. Should you no longer be in your original Scheme, the refund will then go to either to your new Scheme or be paid directly to you. We recommend keeping your PIR information up to date regardless of whether you're joining KiwiSaver self employed, or are switching KiwiSaver companies.

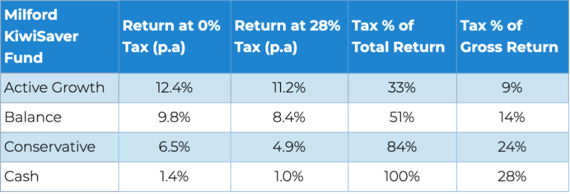

As we mentioned before you only pay tax on the 'taxable portion' of your returns. The difference in the makeup of your fund can play a big part in how much KiwiSaver tax is paid. We did some research to find how much of a fund's returns are made up of taxable income. Using a few of Milford KiwiSaver Plans funds we got an idea of what proportion of these funds returns were taxable. The figures are in the table below.

(Source: National Capital)

As seen above, 100% of the Cash funds returns were taxable - while only 33% of the Active Growth Funds returns were taxable for the period in question. This led to a huge difference in how much of an investor's Gross returns were being paid out in tax.

Depending on how the fund manager has invested your money hence can lead to different tax bills which affect your final payout. So it's good to look into these things. You can check your returns through the Milford KiwiSaver login or other providers' KiwiSaver login pages.

As most KiwiSaver investment options are PIE schemes, investments in some Australasian shares are exempted from tax because of the Foreign Investment Fund rule. Gains on New Zealand shares are also currently tax-free.

The set of rules for companies that meet the Australian company share exemption criteria are as follows:

A company must be included in the official ASX list,

The company is an Australian resident and is not considered a resident of any other country under an agreement reached between Australia and the other country,

The company maintains a franking account, and

The company offers stock that is not stapled.

KiwiSaver providers share with the public and their clients the companies they invest in for the different schemes they have. If you are curious to find out which companies are exempt from paying tax you can access the ASX list and search for the companies shown in your scheme’s list of investments. The investments made on those companies are the ones you are not paying tax on.

The IRD considers this list as reasonable care when taking a tax position. Therefore, you as the investor will not be penalized (will not owe money to the IRD) should changes to this list be made before your scheme provider knows about and is able to take the necessary steps to allow for PIR adjustments.

You can do the same for New Zealand companies and find them on the NZX50 list if you are curious to create a more detailed view on which parts of your KiwiSaver investment are not subject to tax.

The value of this tax-free status is very valuable, particularly for younger investors who may be in KiwiSaver for 30-40 years and so get the compounding benefit of tax-free gains for a long period.

However, tax on other international shares is paid on the income you derive from those shares.

For example, let's assume John’s KiwiSaver scheme has a total balance of $10,000, of which $4,000 are invested in Australasian equities or shares, while the other $6000 are invested in international shares. According to the current taxation rules, the ‘income’ on the $4000 which are invested in Australasian shares are tax-free. However, John will have to pay tax on the ‘income’ he earns from $6000 from the international shares at his PIR rate.

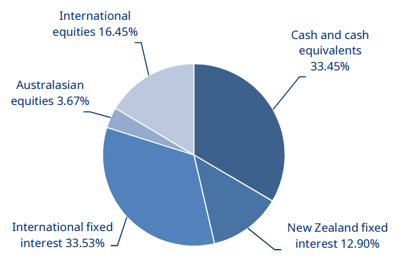

Below is an example of a fund that includes a percentage of the total assets invested in cash, Australasian and international assets to better understand the distribution of assets in KiwiSaver fund investments.

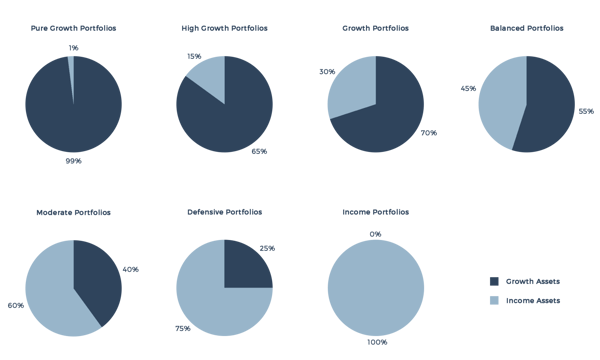

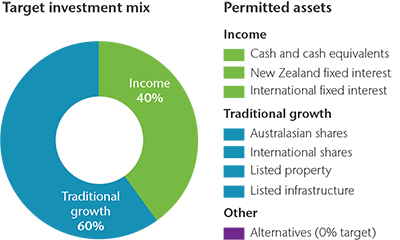

Below figures are an example of how a KiwiSaver schemes allocation with respect to growth and income assets look like.

In most cases, growth assets such as shares, generate more taxable returns as compared to investments in bonds, fixed interest bonds etc. Thus, a KiwiSaver scheme with a higher asset allocation to growth assets is likely to incur more tax as compared to a scheme with more allocation to income investments.

The amount of tax you will be charged thus will not just depend upon how much of your assets are invested in growth funds but also what proportion of your KiwiSaver funds have asset allocation in international shares.

In the case of New Zealand shares, there is also no capital gains tax. What this means is that if you today buy shares in a company such as Air New Zealand and their share price triples the next day, you will not be required to pay tax on the returns you make from that price increase. You would only be taxing tax should you receive dividends from said shares.

Returns made from shares invested in international companies are taxed differently. The FDR (Fair Dividend Rate) method is what is used to calculate the tax applied to international shares that are not listed on the Australian share market (remember, we said shares listed on the ASX are tax-free). The method assumes that the international shares will generate a dividend income of 5%. This is applied as a fixed rate which means that no matter whether the share price goes up or down, you only get taxed on 5% of said share value.

Funds with Growth Assets have higher rates of return, and on average give you higher amounts of income. This does not necessarily mean that the tax you will be paying will also be higher. There are benefits to these growth assets. The returns earned on such investments could well make it worth the investors’ while and far exceed the tax they will be paying. After all, there is a reason these growth asset funds are still around. Depending on circumstances and goals, changing KiwiSaver into a high-growth fund is sometimes beneficial.

The new Financial Markets Authorities regulations on fees are designed to give the investors scale benefits that fund managers themselves receive. The fees that the investors are currently paying are deemed to be too high and the value for money they are receiving is being put into question. The FMA’s aim is to help regulate the market in the investors’ favour by demanding higher returns for the fees the investors are paying to their providers or by having these fees reduced. What does this have to do with tax, you might be wondering.

Well, the new regulations’ purpose is to readjust the fee/returns ratio, while the tax rate rate remains unchanged. Meaning you as the investor might be receiving higher returns and/or paying lower fees to your providers. While the proportion of tax you are paying is directly related to the returns, if you are receiving more value for money from your investments, you would consider the tax you are paying to be worth it.

This means that although Funds with more Growth Assets do see, on average, higher returns and are taxed more heavily due to those higher returns, the benefits you would be receiving from such a fund could far exceed the ‘setbacks’ of a higher tax.

Investment managers put a great deal of focus on making their schemes as tax-effective as possible. They are always adjusting the asset ratios in order to achieve the highest returns possible while allowing the investor to minimise the amount of tax they have to pay to the IRD.

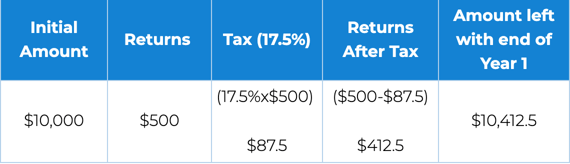

Let’s remember John and his $10,000 KiwiSaver account. For this year he was taxed on all his $500 returns, with let’s say a PIR of 17.5%. Therefore he has $412.5 left to add to his pre-existing $10,000, taking his balance available for investing for the following to $10,412.5.

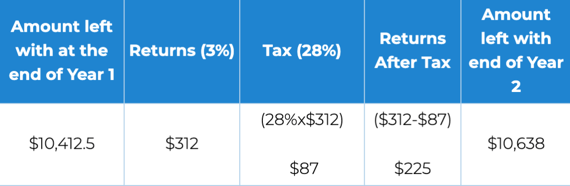

In scenario one this balance earns a 3% return on a Cash Fund composed mostly of investments in Bonds, Term Deposits, and other low-risk securities. This means that $312 (his return on investment 3% x $10,412.5) is being taxed 28% because Cash Funds have the highest tax rate applied to them. This is due to the high allocation of lower-risk securities such as bonds and term deposits. This makes the returns from such a fund much more of a ‘sure’ thing and much more consistent, on average, than returns from other types of funds.

This leaves him with $225 to add to his total amount for his third year of investing.

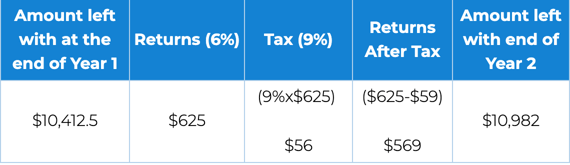

In scenario two he earns a 6% return in a Growth Fund composed mostly of growth assets such as stocks and investment properties. Because he is in a Growth Fund composed mostly of shares and other higher-risk securities, his tax rate (even with a PIR of 28%) has gone down to 9%. This is due to the mixture of securities in a Growth fund, i.e. a mixture of tax-free New Zealand and Australian shares and other International Shares taxed only at 5%. National Capital has run the calculations and the overall tax John has to pay on his Growth Fund returns comes down to 9%.

6% of 10,412.5 is ~$625. The tax on that (9%) is equal to $56, leaving him with $569 to add to his total investment amount for his third year of investment.

So as you can see, that is nearly double the amount he was left with in scenario one.

$569 > $225

Being taxed higher rates on schemes with higher growth asset allocations does not necessarily mean you should shy away from said schemes. I find my KiwiSaver decision-making process is based on a multitude of factors rather than just one single factor.

In most cases, your KiwiSaver scheme is a Portfolio Investment Entity. A PIE is a type of entity (such as managed funds) that invests your contributions in different types of investments as shown in an example below;

Note: For more information on other types of schemes read the additional reading section below.

I can also check the makeup of my PIE find through my KiwiSaver login.

The PIE rules allow investment funds to pay tax on your share of investment earnings at your specific Prescribed Investor Rate (PIR) with an upper ceiling tax rate of 28%.

Since the new legislation in 2019, IRD is now able to give direct instructions to PIE managers to change the tax rate should the Commissioner find that the currently applied tax rate is incorrect. This will be based on the information the IRD has about the investor’s income. It will also instruct the same if you decide to change KiwiSaver to another provider.

Your share of taxable income changes depending on what kind of fund you are in as well as the asset allocation it has.

Paying the correct KiwiSaver tax combined with the right KiwiSaver fund will make a big difference to your KiwiSaver payout.

Spending 10 minutes to complete our KiwiSaver HealthCheck form may be the most important thing you can do for your account right now.