Buying your first home, like any other big life decisions can be exciting but also a little bit daunting. After all, there’s a lot to think about. How to finance it is one of the big questions. If you are a New Zealand resident or citizen living in our lovely Aotearoa and you have been a member for a minimum of three years, all the while actively contributing to a First Home Withdrawal could be an option for you. Before you decide this is the option for you though, we at National Capital have put together a list of pros and cons of using your KiwiSaver to buy a first home. All of the pros are available on the condition that you intend to live in the property that you are planning on purchasing.

Let’s dive in.

Pros

When NZ Super was put in place as a retirement fund the assumption that everyone would own their own home by the age of 65 was also valid. This is no longer the case. So, using your KiwiSaver to purchase your first home can be useful.

Reason 1

Buying a home is considered a very important step towards achieving financial security. Even with the NZ Super rates having risen to $437 per individual living alone, one asks oneself “How am I to afford rent with this?”, when rent prices are so high and always on the rise, it seems. A lot of people’s mortgage payments or rental dues are at least in the range of $400 per week and often above. The average rental price one would expect to pay per week in Auckland is $588. This being the highest in the country. Even somewhere like the West Coast having the lowest rental prices in the country it comes to $264. The prices for somewhere like Northland being the middle of the road rates-wise is still $437 - the whole amount an individual living alone receives from their NZ Super.

NZ Superannuation is very generous by international standards and it does a very decent job at keeping people out of hardship’s way financially - that is if you do not have high housing costs. Purchasing a first home sooner rather than later could potentially protect you from the rising cost of rents as you get closer to retirement. In the last year up to March 2021, surveys conducted on the prices of rental properties on TradeMe show a 6% increase. This is the highest year-to-year increase since 2018. It has only been 3 years since 2018.

Reason 2

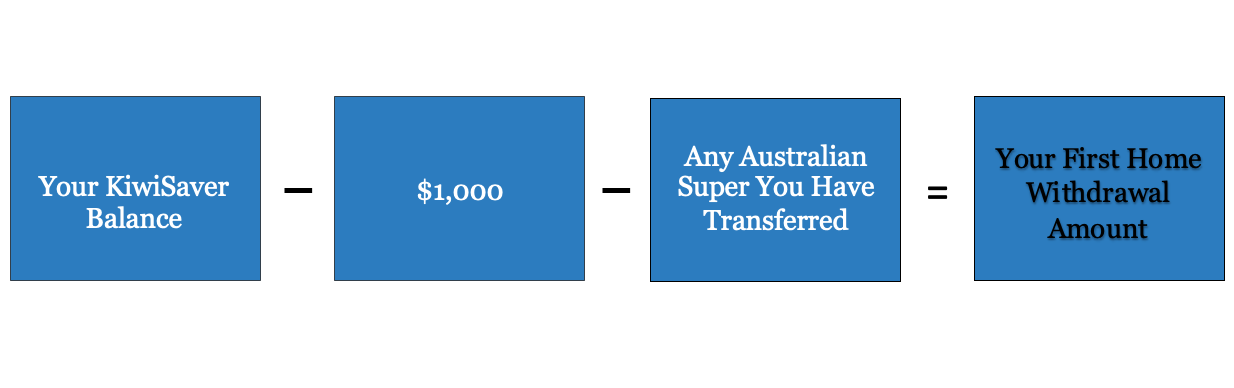

You can withdraw all the contributions you have put in yourself, salary-based and/or voluntary, all your employer contributions, all the government contributions, and any returns gained on all of the aforementioned contributions. You must only leave in the initial $1,000 government incentive which will continue to earn returns as arranged with your KiwiSaver provider.

Reason 3

The low interest rates on mortgage loans at the moment make it very appealing to borrow money to buy a home. Starting from 1.99% for a one-year fixed mortgage loan it is highly motivating to put money towards a first home.

Reason 4

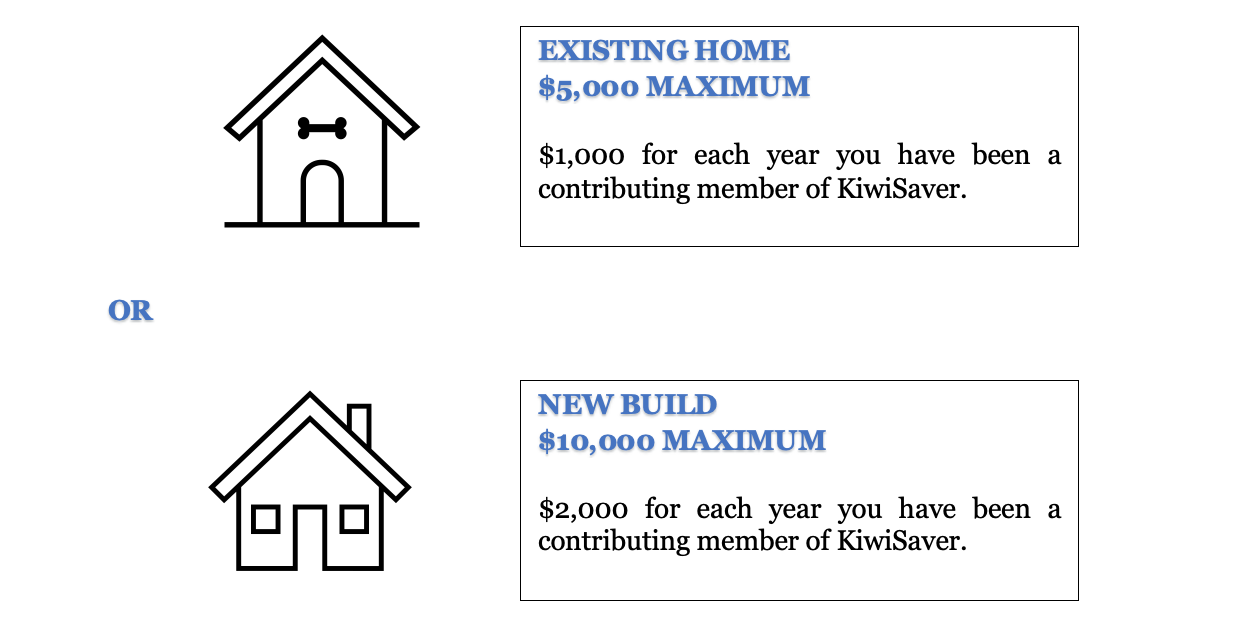

It is possible to attain extra financial support from the government on top of your First Home Withdrawal. It is called the First Home Grant and depending on your income bracket and the type of property you are buying (e.g. plot of land, new home or existing home) you could receive between $5,000 and $10,000 extra to finance your first home.

Reason 5

There are an array of KiwiSaver schemes available that are designed to help first home buyers. National Capital can easily pair you with the right KiwiSaver fund.

Reason 6

There are also the new regulations designed to help first time buyers. If you are to apply for a first home withdrawal you may also be eligible for a first home grant. Single people with a salary of up to $95,000 (before tax) may now use their KiwiSaver money for a full or partial deposit. Couples with a combined salary of up to $150,000 (before tax) are also extended the same benefits. Some major banks such as Kiwibank now accept 5% deposits. On top of that, depending on the type of property you buy, land, a new build or an existing home, you can receive anything between $1,000 and $10,000 to put towards your deposit. There are certain house price caps in place that dictate the type of property you can buy such as a new build or an existing house. For more information you can read our article on New Regulations for First Home Buyers and KiwiSaver Loans. The fact that the government is applying new legislation and looking at building another 130,000 homes across the country to increase the supply could be a very good thing for first time buyers.

Cons:

There are also other things to be aware of that for some might be considered as a downside.

Reason 1

The big one to think about is that taking a large lump sum out of your KiwiSaver account now might mean that you have less money that you originally planned to have when turning 65. Taking the money out can potentially cause worry and stress as to whether you will have enough money to retire on once you reach the age of 65. After all that would be a considerable amount of money you’d be taking out to use on your first home and that money, left in there, would be earning considerable amounts of returns on your investment.

Let’s say Sheila is 30 years of age and has a current balance of $65,000 in her KiwiSaver account. She is in a Growth fund and contributes 3% alongside her employer’s contributions of 3% also. She has a salary of $80,000 per year. If she withdraws $60,000 now to put towards a deposit, with compounding returns, she will have approximately $310,000 by the age of 65.

Now let’s assume she did not withdraw any money for her home. Her current balance of $65,000 will give her about $450,000 by the age of 65.

After years of hard work and dedication to increasing your balance and getting to the healthy savings account that it is now might make it harder on you to consider taking it out and using it to buy your first home. Leaving the money in there does mean you have a higher balance once you retire but that does not necessarily guarantee you a better retirement. You may need to increase your contributions to account for the rising cost of rents in major cities.

Reason 2

With COVID-19’s travel restrictions people are deciding to spend money on buying a home instead. This is good - for those able to get on the property ladder or are already on it. On the other hand, it is important to mention that it has increased the competition in an already lacking market in terms of supply. There is currently still a housing shortage of about 80,000 homes and the increasing demand it could make it harder for first home buyers to compete with second and third-time buyers or developers. The housing shortage has not delivered the drop in prices that was expected last year. The low interest rates and lack of ability to travel and spend money on other ‘frills’ have turned kiwis towards home renovation and property investing. First home buyers may find it harder to collect the right amount of deposit and then make mortgage payments when competing in such a large pool of competitors as they are at times being forced to spend more money than they originally intended to. A survey conducted on approximately 1300 people found that 35.2% of respondents planned on spending money on home renovation and a second survey found that 20% of applicants were planning on purchasing a property, highly increasing the demand for houses.

Reason 3

Buying your first home and taking on a mortgage is a large financial commitment. It might make you feel as though all your financial efforts should go towards repaying your mortgage and you may no longer be able to contribute to your KiwiSaver or at the very least you may not be able to contribute as much as you did before. This might cause you to worry that you will no longer be able to retire at a comfortable level.

You have a house - don’t stop contributing

National Capital says that it is important to continue to contribute if you decide to buy your first home with the current balance. You may reduce contributions if needed to pay down the mortgage but don’t stop entirely.

Cost of living increases makes it harder to take on a mortgage and continue to contribute regularly, especially if the increase in wages does not make up for the increase in living expenses. On the other hand, this could be seen as a pro to using it to buy a first home as well. As we mentioned above, owning a home is considered s one of the most important steps to financial stability. Therefore, despite the rising cost of living, going through some difficulty in the present might be well worth the effort when it comes to retirement. Yes, you read that right. We understand that maintaining a mortgage and supporting a lifestyle while at the same time maintaining contributions to your KiwiSaver account can be a stretch. This quarter alone rent prices rose by 1%, the highest quarterly increase all year. Petrol prices rose by 7.2% and transport prices rose by 3.9%. It is a stretch that should be considered thoroughly and absolutely seek the advice of a qualified financial advisor before signing up to anything. What we are saying is that when it comes to retirement, especially if you are in your 20’s or 30’s now and retirement is a long way away, that house you are buying now could be a real asset to your golden years. It means that as you get closer to retirement you have the opportunity to downsize your home. This will free up a considerable amount of extra cash that you can add to a now healthy-again sum (because you kept contributing) to fund the golden years with.

Further Information for people who have owned property before but no longer do:

It is important to be aware that you can also use this withdrawal option if you have owned property before. Yes, that’s right, you can have owned property before and still potentially qualify for a First Home Withdrawal. The condition is that you must no longer have any interest or shares in the property you bought before and your current financial situation is similar to that of a first home buyer.

For example; someone who owned property before and sold or gifted the property to a second party. The profits from the said property could have been put towards a business venture that did not pan out, medical fees, paying study fees, supporting themselves through study, or used to support their family. The financial situation of the first party could be considered similar to that of a first home buyer. They may have enough capital left for a partial sum of the deposit or no capital at all and need their balance for the full required amount as they attempt to scale the property ladder.

Applications must be lodged with Housing New Zealand and eligibility is determined on a case by case basis.

In order to qualify, you must not have retrieved funds from KiwiSaver before and you need to have been a member for at least three years. This part is the same as for all other first home buyers. Your total of realizable assets must also not equal more than 20% of the house price cap for existing properties in the area that you are looking to buy in. For more information on what Kainga Ora means by realizable assets and retrieval of application forms, you can visit their website. If you are eligible for withdrawal, your letter of acceptance coming from Kainga Ora must also be presented to your scheme provider and follow their instructions regarding the withdrawal of funds.

How can I access my KiwiSaver money should I want to?

In order to access the money in your scheme, you need to request a letter from your provider that confirms you are eligible to withdraw your money and put it towards your First Home Deposit. You will then need to request a withdrawal form from your provider which you will have to go through with a lawyer and sign it in front of them. This last procedure can go on for up to 10 days so it is important to have things in order before the settlement date.

The money then gets transferred from your provider to your solicitor and is kept in a trust account until you need it. It is from this trust account that is then transferred to the trust account of the vendor’s lawyer waiting for the finishing touches of the sale to take place.

You might be wondering what happens if for whatever reason the sale does not go through. In such a case, your solicitor will send the money back to your KiwiSaver scheme manager’s account and you may be able to apply for another withdrawal at a later date.

Some Final Advice

Instead of thinking of it as either owning a home or having a better retirement, think of it as either investing in property or into a managed fund. Either way, talk to a professional so you understand both options. Make sure that you have considered all pros and cons, including how much you should put towards your first home, how much you’d like to have by the time you retire and how much contributions you should put towards it in order to achieve your goals.

There are several different providers whose schemes are designed to cater to first home buyers. National Capital can match you with one of those providers. Depending on when you plan on buying your first home there are a few things to consider such as the amount of risk you can take on. Start by taking our KiwiSaver HealthCheck and find out which provider is the best for you.

Some people will be retiring now and in the near future, some will be retiring in 20 or 30 years' time. However, if you are in a group of people who do not own their own home or have no foreseeable chance of owning a home, this could affect your retirement goals in a considerable way. While you may not have a house of your own, your pool of money by the time you retire might be larger than that of those who opted for the option of using their KiwiSaver at some point to purchase a property. National Capital can help you make the most of your savings no matter what your financial goals are. The Healthcheck can be taken by anyone and it’s free advice, so wait no longer.