So what is Diversification?

Diversification is a risk management strategy that mixes a wide range of investments within a portfolio. Diversifying involves investing in differing asset types and investment vehicles to limit risk from any single external factor. Investments can include, but aren’t limited to equities, property, fixed interest and cash. This investment strategy protects the portfolio and lowers the risk of any individual holding or security while also yielding higher long-term returns.

Do all KiwiSaver Providers invest the same?

The short answer is no. There are minor discrepancies between all KiwiSaver providers; this is why we see differences in the returns. These investment strategies can vary depending on what KiwiSaver Funds you are looking at as well. Conservative and Moderate Funds tend to have a majority of their investment mix in Income Assets. Income Assets are investments such as cash deposits with banks, bonds issued by Governments, councils and companies to fund projects. Income Assets are seen as low volatility investments because they have other pay distributions. Hence, investments see more stable returns, but this doesn’t mean that returns can be negative.

On the other hand, KiwiSaver Funds such as Balanced and Growth Funds have most of their investment mix in growth assets. Growth Assets can be shares in large companies, such as Apple, Microsoft or Amazon. Other investments also include companies investing in and developing property, such as buildings, shopping malls, and hotels. As a result, growth Assets show higher volatility compared to Income Assets. They tend to experience more noticeable rises and drops in value.

Growth Investment mixes from KiwiSaver Providers

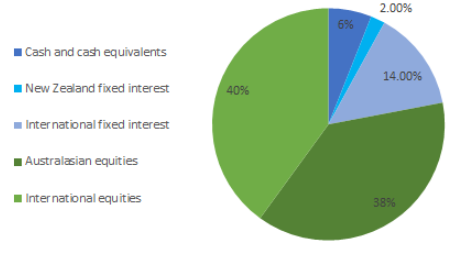

Below, we see the Growth Fund target investment Mixes from ANZ, Booster, and Milford as of September. We see that most KiwiSaver providers follow a similar investment mix between income and growth assets to ensure the fund is secure. Below also shows the specific areas in which they invest.

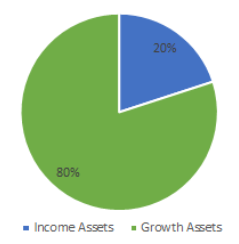

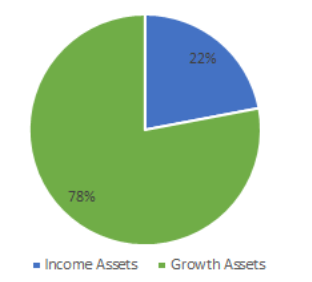

ANZ Investment Mix

To find out more about how ANZ performs, check out our blog on ANZ’s KiwiSaver performance in August.

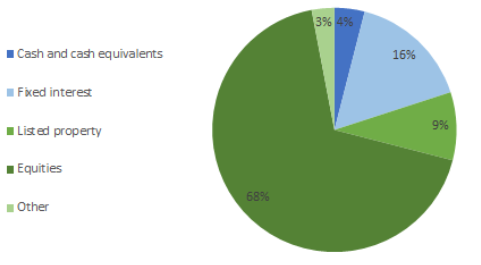

Booster Investment Mix

To find out more about how Booster performs, check out our blog on Booster’s KiwiSaver performance in September.

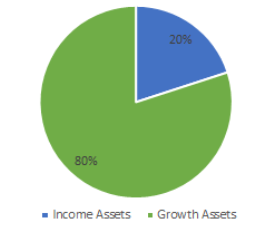

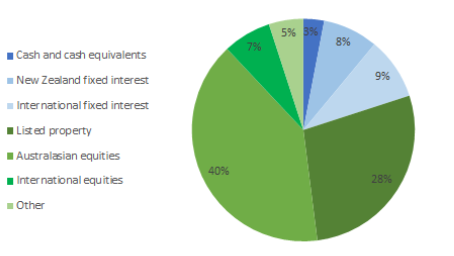

Milford Investment Mix

To find out more about how Milford performs, check out our blog on Milford’s KiwiSaver performance in September.

Comparing these KiwiSaver Funds

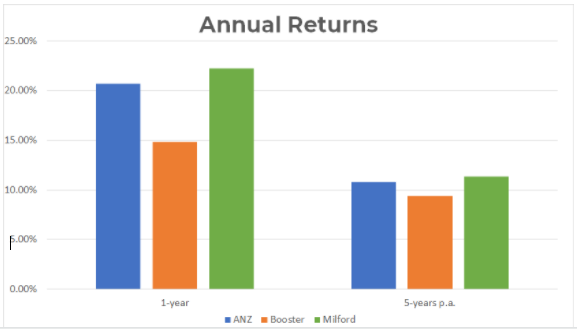

Above see how, although they invest quite similarly within growth and income assets, the target investments vary differently between them. Milford’s Growth Fund even has less invested into growth assets than the other two, but does this mean that it performs any less? In actuality, just because a fund has fewer growth assets does not mean it will perform any less than other funds. Below, we see the one-year returns and the five-year average returns of all three KiwiSaver providers. As we can see, Milford has outperformed both providers while having 2 per cent less invested in growth assets, which shows that ANZ and Booster have more volatility than Milford while still making fewer returns. As an investor, always remember that just because an investment may have higher volatility doesn’t mean that it will perform higher than other less volatile investments.

Returns for Growth Funds

|

1-year |

5-years p.a. |

|

|

ANZ |

20.71% |

10.77% |

|

Booster |

14.80% |

9.40% |

|

Milford |

22.21% |

11.36% |

If you want to see how these providers compare with others, you can view a list of the best KiwiSaver funds here.

What to take Away

Diversification is a fantastic tool used throughout investing, not just KiwiSaver. By taking the time and effort to choose investments carefully, a portfolio can outperform better than those with more volatility. By diversifying your assets into 20 or 30 investments, you can have some cushioning if some shares have a drop, as the others would outweigh it. Having investments in multiple sectors allows them not to be affected by similar external factors. By only having 20 to 30 investments, you can manage them with some ease instead of having too many and not being able to keep track of them.