A lot has happened during the last few years. You may have noticed your KiwiSaver investment go through a rollercoaster ride at the same time. Above all, I want to point out that the investment volatility you experience is normal during times of global instability.

This article aims to analyse the impact of global markets and events on KiwiSaver volatility. Firstly, we will discuss the make-up of most KiwiSaver funds on a macro level. We will also be looking at industry-specific volatility, global uncertainty, and recent events.

Moreover, we discuss diversification as a technique used to reduce risk and why we should have a positive outlook for the future. As our initial instinct in unstable times is to buckle down and disinvest, share markets take a tumble. However, historical data tells us that long-term investments are able to weather any short-term instability. This is partly the reason why withdrawing your KiwiSaver funds is restricted under only a few circumstances. Generally, a 30-year investment has seen substantial growth to the point where the impact of short-term volatility isn’t a major concern.

It’s important to make investment decisions with a clear head and without undue stress as a result of market conditions. National Capital offers a Free KiwiSaver Healthcheck based on your specific goals and risk tolerance backed by historical data. So, before considering the idea to switch KiwiSaver, you should ask yourself, “Am I doing it for the right reasons?”

The make-up of your investment

The majority of KiwiSaver providers offer a range of funds based on your risk appetite. As the saying goes, “higher risk is associated with a greater probability of higher returns”. Funds are typically made up of a mix of income assets and growth assets. According to the ASB KiwiSaver offering, income assets include things like cash deposits with banks, and others like government bonds. Growth assets are shares in large listed companies (like Apple, Uber, Meta), which tend to be more volatile.

Cash and Conservative Funds are typically the lowest risk funds. Cash funds normally invest in NZ-based income assets with little chance of negative return. According to Morningstar, investors have seen between 0.9% and 1.9% returns per annum in the last 5 years. Conservative funds aim for an 80/20 split of income/growth assets. They have offered an average 4.9% per annum return in the last 5 years. Conservative funds are more exposed to global events than cash funds as they include more international investment.

Moderate and Balanced Funds can be seen as mirror images of each other. Moderate funds aim for a 60/40 split of income/growth assets and balanced funds aim for 40/60. Generally speaking, funds with a higher percentage of growth assets are exposed to a higher level of international equities. In the last 5 years, the KiwiSaver provider average has been 6% return per annum for moderate funds and 8.4% for balanced funds.

Growth Funds are a mirror image of conservative funds and aim for a 20/80 split of income/growth assets. In the last 5 years, the industry average is a 10.8% return per annum. Typically, growth funds are the most exposed to international equities and volatility.

Industry-specific volatility

Although global events generally impact the entire share market to a certain degree, some industries are more exposed than others.

A perfect example of this was the airline and travel industry during the start of the Covid-19 pandemic. The S&P 500 is a stock market index tracking 500 of the biggest companies listed in the US. Between February 21 and March 20, 2020, the S&P 500 index decreased by 30%. During that same period, Hilton (hotels) share price decreased 43.8%. Delta Airlines share price decreased by 63.1%. The lockdowns meant that revenue in the transport and travel industries almost came to a halt overnight. As a result, investors sold their shares in such companies and their stock prices tumbled significantly.

Therefore, some KiwiSaver providers were able to navigate those early pandemic wobbles better than others depending on their prior exposure to such industries. For example, my personal KiwiSaver investment in the Milford Aggressive Fund decreased 24.95% within that same period. Although it’s never great to see, it outperformed the S&P500 index which indicates less than average exposure to the companies that got hit the hardest by the pandemic.

Global uncertainty and recessions (GFC 2008)

The World Bank tracks global economic data to record past fluctuations and project future growth. Thus, helping decision-makers minimise the impact of uncertainty in the future. The 2008 Global Financial Crisis (GFC) was a worldwide economic crisis that saw GDP shrink by 1.7% in 2009. This downward trend in production and employment over an extended period of time is called a recession. Typically, a drop in production and employment equals a drop in confidence for the future outlook of most companies.

Thus, with investor confidence dropping, so do their investment funds. It is a classic example of supply and demand. When there are more sellers than buyers in the market, the value of that particular stock drops. That is exactly what happened to most investment funds during the GFC. Although some markets were impacted less than others during this particular period.

As you will see on the graphs below, the NZX 50 Index was less impacted than the S&P 500 Index. What this means is that if your KiwiSaver Scheme was investing a big portion of your savings in NZX 50 companies, you were better off at the time. Generally speaking, investments in ASX 200 and S&P 500 companies equaled bigger losses or lower returns during that period.

The takeaway here is that global financial and employment struggles often negatively impact your KiwiSaver balance. Depending on the make-up of your selected fund, your investment may be more or less exposed to the fallout.

KiwiSaver Fund Diversification Strategy

By accessing your fund details through your online KiwiSaver Login you will be able to see your investment portfolio. You will notice that your funds are invested into tens if not hundreds of companies in multiple industries.

For example, up until 28 February 2022, Milford has invested my funds in various types of assets:

- Effective Cash = 14.19% of fund.

- New Zealand Equities (local growth assets) = 5.43% of fund.

- Australian Equities (international growth asset) = 17.66% of fund.

- International Equities (international growth asset) = 62.67% of fund.

Moreover, my investment in the Milford Agressive fund is also split accross multiple industries:

- Information Technology = 17.46%

- Financials = 16.07%

- Health Care = 10.57%

- Consumer Discretionary = 8.88%

- Industrials = 7.95%

- Communication Services = 6.36%

- Consumer Staples = 5.35%

- Energy = 4.39%

Furthermore, the same fund can be classified by region exposure:

- United States = 48.48%

- Australia = 16.94%

- Europe = 8.08%

- New Zealand = 5.00%

- Other Countries = 3.06%

- China = 2.03%

- India = 1.18%

- Japan = 1.04%

- Cash and Other = 14.19%

Different funds and schemes will have different combinations of exposure to different market forces. KiwiSaver providers hire some of the top financial managers and teams in the country to find the best combination possible. However, investing in the stock market is unpredictable, and that is the reason why portfolio managers diversify our investments. The perfect analogy for diversification is the opposite of putting all your eggs in one basket. You’re investing in different baskets of all shapes and sizes so that you’re not left exposed if one gets damaged.

The bright side

Despite all of this talk of instability, recessions, and negative return, there is light at the end of the tunnel. History will tell us that if you’re in it for the long run, your investment will have a positive return. Let’s take a look at some major market indexes in which many KiwiSaver providers invest in.

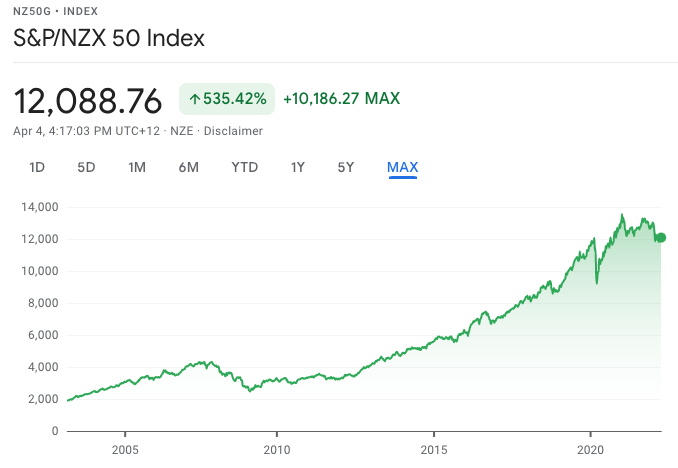

NZX 50 Index - Since March 21, 2003

Source: S&P/NZX 50 Index by Google Finance.

There are clear signs of the NZ market index volatility if we zoom in at certain moments in time. However, the market has grown 535.42% in value since March 21, 2003.

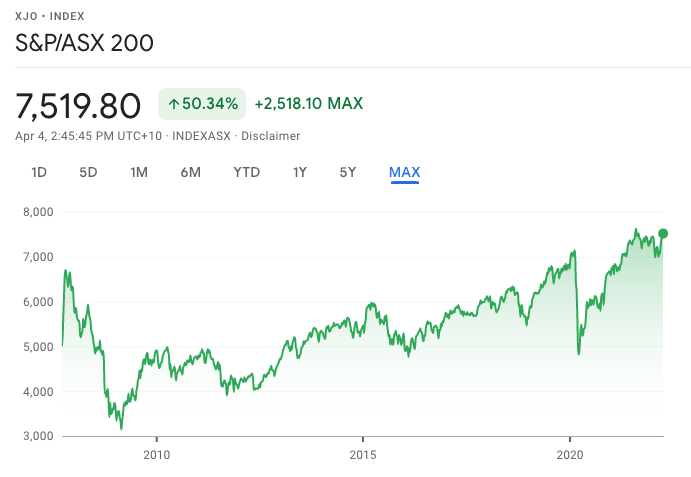

ASX 200 Index - Since May 31, 2006

Source: S&P/ASX 200 Index by Google Finance.

The Australia stock market index fund shows much more volatility than the NZX 50. Although, yet again, since May 31, 2006, the market value has grown 50.34%.

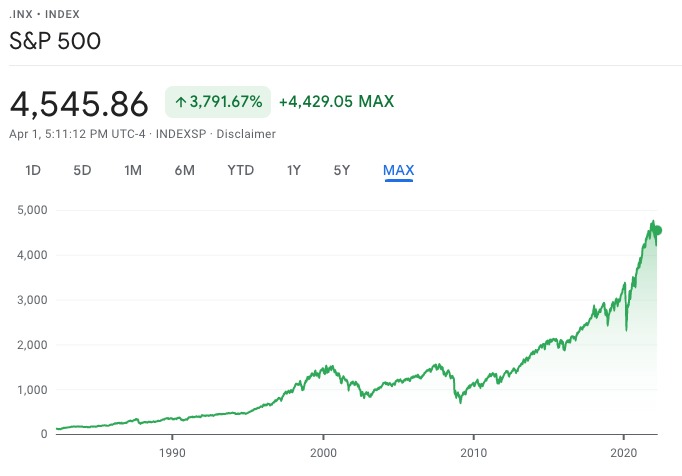

S&P 500 Index - Since April 16, 1982

Source: S&P 500 Index by Google Finance.

Incredibly, the S&P 500 index has grown 3,791.67% since April 16, 1982.

Therefore there are two main takeaways from these historical graphs that are valuable for every single KiwiSaver member. Global events such as the GFC and the Covid-19 pandemic have a direct negative impact on major funds and companies. Secondly, and most importantly, long-term investments have historically proven to yield high returns despite volatility along the way.

Changes in times of instability?

The FMA found that between February to April 2020, switching KiwiSaver was 3x higher than normal. As we previously touched on, this was the beginning of lockdowns and the start of the Covid-19 pandemic. What’s interesting is that younger members aged between 26 and 35 made 5x more switches than usual.

We can safely assume that the reason why younger people are more likely to react to turbulent times is due to the lack of exposure. By that, I mean that older generations have experienced more times of instability than younger people. And with experience, comes greater composure in dealing with volatility and times of uncertainty.

If history tells us anything, it is to hold your nerve. When my KiwiSaver balance took a 24.95% dip at the start of the Covid-19 pandemic, I decided to do absolutely nothing. Why?

Let’s look at my options. I was already in an aggressive fund with high risk and market volatility. When I lost 24.95% of value in what felt like overnight, I could have switched to a less volatile fund. Although, as we mentioned, the average return per annum in cash and conservative funds is between 0.9 and 4.9%. Meaning, it would have taken me years to get my investment back to pre-pandemic levels.

Instead, I decided to stick with the Milford Aggressive Fund, although, in all honesty, I was certainly sweating. However, I was reassured by the fact that stock market history tends to repeat itself. There are ups and downs, but in the long run, it trends upwards. Since February 21, 2020, I have seen my investment fully recover the losses and gain an additional 9.71%. Thus, my takeaway is to make investment decisions based on your personal circumstances and goals, rather than volatility and fear.

Conclusion

Without a doubt, negative global events such as war, pandemics, and financial crises, have a negative impact on KiwiSaver funds.

Different industries and locations may have varying levels of exposure to such negative events. For example, during the Covid-19 pandemic, air transport and travel industries were one of the hardest hit, globally. In another case, the Global Financial Crisis (GFC), had a much more negative impact on the S&P 500 than the NZX 50.

All KiwiSaver providers apply a diversification strategy particularly to limit the funds' exposure to any type of crisis. This is done through investment in different countries, asset types, and industries.

Lastly, despite the real possibility of losing money on your investment, history tells us there is a bright side. Long-term investments in the NZ equity market, as well as overseas, have a track record of significant returns despite volatility along the way. There are times when switching KiwiSaver is the right call, based on your lifestyle and goals. However, switching between funds and providers due to instability may lead to a worse outcome than staying put.

If you have any questions about KiwiSaver, you can complete the National Capital Free KiwiSaver Healthcheck. One of our financial advisors will get in touch and discuss the best solution available for you.